One of the Best Businesses Ever Conceived: Rightmove

$RMV $RTMVY

If you live in the UK you will most certainly know this company because it is practically impossible to buy or sell, or rent, a house without interacting with Rightmove.

Founded by several of the leading real estate agencies in 2000, Rightmove is by far the country’s largest online property portal.

According to the company, consumers spent 16.4bn minutes on its site in 2024. There are roughly 54m adults, so that is 5 hours per man or woman in the UK annually. That equates to an 85% market share.

And it shows up in the numbers. Rightmove’s gross margin is 100% (doesn’t get better than that!) which they convert into a 70% EBIT margin.

Further, they employ almost no capital in operating the business. Their £390m of sales are supported by £119m of assets, of which £41m is cash. There is so little capital employed in the business that a return on invested capital (using the UK’s 25% tax rate) in 2024 was an implausible 460%.

Divided by a Common Language

And this is why, despite my predominantly American audience, I hesitate to call Rightmove “the Zillow of the UK”. Because this does a serious disservice to Rightmove. Since for all Zillow dominates the US property search market, its financials could not look more different.

Far be it from me to question the strategy of legendary CEO Rich Barton (he also co-founded Expedia and Glassdoor before stepping down from Zillow a year ago), but in contrast to Rightmove’s lean cost structure, Zillow spent $585m on R&D in 2024, or 26% of sales, so pretty much the entirety of Rightmove’s cost base. Further Zillow expensed $448m of share-based compensation for employees. Yes, there will be some overlap between these two numbers but nonetheless these expenses are enormous. Rightmove expensed £7m ($9m) of share-based comp.

As a result, Zillow is consistently loss-making.

There are also two crucial relevant differences between the US & UK property markets. The first is that Multiple Listing Services (MLS) don’t really exist in the UK and the second related point is that home searchers very rarely use a buyers’ agent.

In the US there are over 500 MLSs owned by associations of realtors. A California realtor will belong to, and pay dues to the California MLS in exchange for access to property listings and the ability to list homes. Zillow and Homes.com pull data from these databases to populate their sites. Realtors will primarily use the MLS to search for listings for their clients and get additional data about the property (including the commission they’ll earn!).

In the absence of an MLS, Rightmove effectively acts as the centralized repository of listings in the UK. This much more deeply entrenches Rightmove in the property transaction process. You can sell a house without using Zillow but it is much more difficult to do so without using Rightmove.

Because there is no buyers’ agent in the UK, the way Rightmove gets paid is quite different. Zillow is primarily paid for generating a lead for the buyers’ agent (when you click to tour a property they will put you in touch with a buyers’ agent not the listing agent). Prospective buyers’ agents will pay thousands of dollars a month for these leads.

By contrast Rightmove primarily gets paid in the form of membership fees paid by each estate agency office. CoStar argues this is a far superior model and employ a similar model at Homes.com (the principal competitor to Zillow in the US who we will meet below)1.

While, as we will discuss below, Rightmove has formidable advantages on both sides of the network: both in terms of buyers and in their inventory of homes, in Zillow’s case they only really have an enduring advantage in the former because any challenger can pull the same listings data from the MLS.

Why does this opportunity exist?

This is a company used every day by many Brits, it’s hardly undiscovered so why is the stock compellingly valued?

Well, the UK stock market is one of the most structurally unloved on the planet. Most markets have a distinct ‘home bias’ in that local investors and institutions are heavily weighted towards domestic assets for various reasons. By contrast there are several reasons why this is not the case in the UK.

One, investors pay a 0.5% ‘stamp duty’ or sales tax on individual stock purchases, a tax that applies to UK-listed companies but not overseas equities, so local shares are disadvantaged.

Two, according to Seeking Alpha, domestic pension fund ownership of UK stocks has fallen from 73% to 27% of assets from 1997 to 2021. This is because these funds are largely closed to new investors so the beneficiary pool is aging and thus the funds have correspondingly moved into lower duration assets like bonds.

Third is performance. A domestic investor in the FTSE100 blue chip index has made 25% over the past decade (ex dividends). By contrast in Sterling terms an investment in the Nasdaq has returned 336%! Ultimately most investors chase performance.

Hence many of the most popular companies in the UK have either moved their listing or gone public overseas, including Flutter (the owner of FanDuel) and Arm Holdings.

As a consequence, smart money (private equity ) has been buying up UK public companies. For example, Hargreaves Lansdown, the UK equivalent of Charles Schwab, was taken private by a group of PE firms in combination with one of the company’s founders earlier this year.

Indeed, Rupert Murdoch’s REA Group (an Australian property portal) bid for Rightmove in 2024, making 4 offers to buyout shareholders. The most generous was £6.2bn ($8.3bn). These offers were – fortunately - rebuffed by Rightmove’s board.

Competition

Another stock specific reason for Rightmove to be reasonably valued is perceived competitive threats. With 85% market share there is a danger that the only way is down! However, this is an industry that tends towards monopoly and Rightmove has proven very difficult to unseat.

There have been many pretenders over the years.

Originally the competition was traditional print media where estate agents would advertise their listings. This was not a fair fight as the return on ad spend listing on Rightmove proved far higher than ads in local newspapers, which in many cases made their way straight to the trash.

Zoopla was founded in 2007 by serial entrepreneur Alex Chesterman. In subsequent years it bought up a number of competitor sites including Thinkproperty.com from the Guardian newspaper group, and Daily Mail group’s FindaProperty.com and Primelocation.com. Zoopla was bought by PE firm Silver Lake Partners for $2.2bn in 2018 and remains Rightmove’s principal competitor.

In 2009 Google began scraping property portal websites to make listed properties available on Maps. Google withdrew from advertising properties in early 2011. Rightmove partnered with Maps to power their map feature.

The latest competitor is On The Market, which was launched in January 2015 by a group of the largest real estate agencies in the UK with a view to fighting the dominance of Rightmove. The company went public in 2018 but was not a success and was sold to US behemoth Costar Group for £100m in October 2023.

Costar is a behemoth with deep pockets and a $31bn market cap. The company set its stall out in announcing the purchase: “CoStar has a track record of acquiring… property portals that are not the number one players and investing and building them into the most successful portals serving their market. CoStar Group acquired 5th place US residential rental platform Apartments.com in 2014 and grew into the number one player in the US… CoStar Group recently acquired Homes.com, a 6th place residential property portal in the US… and turned it into the fastest growing US residential portal with more than 100 million unique visitors in September of 2023. Homes.com is now the number two most trafficked residential marketplace in the US.”

And they are pleased with their initial results:

That said, catching Rightmove is a daunting task due to its powerful network effects and that is why they have seen off all previous challengers. Rightmove is the first port of call for home buyers, who come for the widest selection of properties, which list on Rightmove to be seen by as many customers as possible. You can see how the virtuous circle spins. 85% of customers access Rightmove directly via the app, rather than via Google.

According to Best Agent, Rightmove currently has 1.2-1.3m listings (for sale and for rent), Zoopla 1-1.1m and On The Market 500-700k. There will be significant overlap with many properties listed on Rightmove and one other portal. For example I searched £2m homes in SW5 (a West London post code). Rightmove had 13 listings, while On The Market had 11 of which 8 were common to both.

However the clearer evidence for Rightmove’s dominance is on the consumer side of the flywheel. Per Similarweb data, in the most recent month, On The Market had 17m visits, Zoopla had 29m and Rightmove had 87m. So an estate agent may choose to list on Zoopla and Rightmove, but they will not list solely on Zoopla.

Business Economics

There are 1-1.2m residential sales annually in the UK, roughly ¼ of the US market, so this is a large market and Rightmove represents an effective toll on transaction activity.

As above, Rightmove gets paid in the form of membership fee paid by estate agents’ offices. Average revenue per agency (ARPA) is £20k a year. There were 1.1m property transactions nationally in 2024, while the median house price was £290k. The average broker commission is 1.5% (including tax) so 1.2% net – another big difference vs the US!

So the revenue pool of broker commissions is £3.8bn. Let’s say there are 20k agencies (Rightmove has 19,000 as customers). So on average an agency is making £190k annually, of which they are paying nearly £20k to Rightmove or roughly 10%. This may seem on the high side, but viewed in the context of a monopolist network like the App store (30%) or Uber (29%) probably about right and may even have scope to rise over time.

This analysis excludes the rentals side of the business which is a smaller but more steady profit pool. A little under 20% of Rightmove’s total listings are rentals. These will be lower priced, higher turnover listings so 15-20% is probably a good approximation of rental contribution to sales.

As a result of the subscription model, Rightmove is not particularly sensitive to property prices or even transaction volume. Sales only drop – as was the case in 2009 and 2020 – when business is so bad that agencies actually go out of business. In 2020 Rightmove did their best to avoid this by offering substantial discounts on membership fees (75% from April to July 2020) which they slowly withdrew through the year.

Scrolling Back & Forward

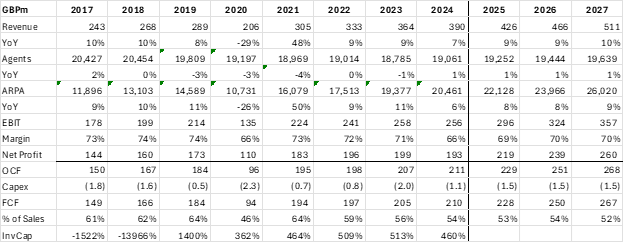

Below you can see the historic numbers and some projections:

Analyst projections are right in the middle of the company’s guidance for 8-10% revenue growth and an EBIT margin of 70%.

You can see the fabulous economics of the business with 70% EBIT margins, free cashflow (FCF) margins north of 60%, and extremely high return on invested capital (ROIC) figures. The negative ROIC numbers are because in the 2015-2018 period the denominator was negative, i.e. in accounting terms there was no invested capital. So the negative numbers are meaningless but I leave them in to highlight the point of how little capital this business requires.

Unfortunately the company’s very high growth phase is over. You can also see that the number of real estate agents has been broadly flat for many years in the UK. One of the reasons for this is that the number of property transactions in the UK has been flat to down as you can see below:

I have also shown in this chart that the government has tweaked the Stamp Duty rate in recent years by offering reductions to try to boost transaction activity.

Somewhat uniquely, UK property owners don’t pay an annual property tax, they pay an upfront sales tax, called Stamp Duty. This effectively reduces transaction activity as there is very little holding cost but a high transaction cost. For a £1m home this currently works out to just over 4% and is typically paid in cash on top of the deposit you have to raise to buy the house.

While an annual tax would make a lot more sense, particularly to Americans used to this system, this would be a big change for Brits and likely would be fiercely resisted.

In any case what this has meant for Rightmove is that in the absence of customer (realtor) growth, the company has had to charge more per Agency. You can see in the original chart that this has been growing at high single digits. A growth rate this high potentially risks annoying their customer base (estate agents), ill-will which no doubt On The Market and Zoopla will try to exploit.

Capital Allocation

One of the biggest risks with a fabulously high return on capital business is that they throw off lots of cashflow and have few organic options to reinvest this cashflow at comparatively high rates. Management teams are typically incentivized to grow their empires which often leads them down the path of poor acquisitions, new business lines and new geographies.

Fortunately Rightmove has gotten into the habit of returning pretty much all the cashflow it generates to shareholders, principally in the form of buybacks and to a lesser extent dividends (in the interests of conservatism they cut the dividend and reduced buybacks in 2020):

A Short Diversion on Buybacks – feel free to skip ahead

This is where a company uses its own cash to buy its own stock. Let’s say a company has 100 shares. It uses its cash flow to buy (and cancel) 3 of those shares. Now the owners of each of the 97 remaining shares have a claim on a higher proportion of the company’s assets/ future cashflows (1/97 instead of 1/100).

Buybacks are not always a good thing, as firms often execute them procyclically, i.e. when their shares are expensive (relative to the intrinsic value of the company). This is somewhat inevitable since when a company is generating lots of cash flows to pay for buybacks its stock price is generally riding high.

And it is partly a principal agent problem as CEOs are incentivized to get their share price up - so a price insensitive buyer helps - and to maximize earnings per share (EPS), where a lower denominator is useful.

But in short if you buy a share below intrinsic value you are creating value and above intrinsic value you are destroying value. The further from intrinsic value the more value you are creating/ destroying. The problem is that intrinsic value is inherently difficult to calculate, depending as it does on unpredictable future cash flows.

Back to Rightmove & Valuation

In Rightmove’s case they are buying pretty consistently and I happen to believe the business is reasonably valued so I am perfectly happy for them to be buying stock with my cashflows. Less rationally, I also quite like that I get a daily press release telling me that the company has bought back a few shares so my ownership continually rises.

As to valuation, the market expects £267m of free cashflow in 2027, which I suspect is on the low side as it reflects the lowest FCF margin aside from 2020 since 2008. I believe they can do £280-300m.

I think you could conservatively pay 25x FCF for a business of this quality with roughly 10% growth. That’s worth a little north of £10 a share or 33% upside to the current share price plus a few dividends. For US investors, the ADR equivalent price is $27.40.

As a sense check, leading PE firm EQT acquired Property Guru - the dominant Singaporean property portal - in late 2024 for 44x OCF while Zillow is presently valued at 56x FCF, and REA Group 50x FCF.

Risks

Firstly this is a business that wholly operates in His Majesty’s Pounds Sterling so to the extent that an investor thinks and transacts in another currency, the fluctuations of £ are a risk.

Secondly as discussed Rightmove is not particularly sensitive to property values and transactions but in a recession or property collapse the company clearly will not hit that 10% revenue per agent growth number. It is a monopolist but has to be somewhat sensitive to its customers challenges.

Finally, while capital allocation has been excellent to date, the company has no controlling shareholder to police this and management teams always reserve the right to start doing stupid things! Using our cashflows to buy up an Italian car buying portal (for example) may be a great idea, or may not be!

I believe the opportunity to own such a high quality company at an acceptable valuation compensates for these risks, BUY!

Thanks for reading, as always please share! This is my second largest public equity holding so I would love feedback!

Disclaimer

This article is purely for informational and entertainment purposes and should not be construed as investment advice. Please consult a financial advisor before making any investment decisions.

Please also assume that I own and intend to trade any stocks discussed before and after dissemination of this report.

1Homes.com open letter: Home Sellers and Listing Agents Matter | Homes.com

Any idea who in particular and why someone on the Board/Exec said ‘no thanks’ to Waystar Royco’s offer, ditto who/why they haven’t bought an Italian car buying portal or similar?

Are chairperson/CEO statements interesting in this regard (or any regard!) or just the usual AI-generated twaddle.

Thanks v much!

I agree that it would be a disgrace to call Rightmove “the Zillow of the UK”. This is such an interesting company. Thoroughly enjoyed the writeup. Different kinds of business but reminds me of Booking and OTCM in some aspects. Certainly didn’t know about the differences btw US and UK real estate transaction industries. Thank you. 10% might sound high but this is probably just though of as the cost of doing the business. Wonder what the churn number looks like. The infinite ROIC and the straightforward capital allocation certainly makes the valuation simpler. 4% FCF yield doesn’t seem like a rich valuation if it can grow at 10%. Thank you for the idea!