Let’s start with a quick trivia question. Over the past 5 years which has been the best performer out of the Mag7 (Amazon, Apple, Google, Meta, Microsoft, Nvidia, Tesla) and Altria (the owner of the Marlboro brand in the US)?

Of course it’s Nvidia (+1070%), what are you crazy?! But in a respectable 5th place, beating out Amazon (+47%) Microsoft (+60%) and Meta (+77%) is Altria with an 82% total return.

What explains this, has there been a sudden resurgence in smoking in the US? Quite the contrary Altria saw volumes decline at a 9% CAGR from 101bn individual cigarettes sold in 2020 to 62bn in 2025. Altria has no material vaping angle either. Pricing partly made up for the volume decline but not nearly enough to grow sales which declined at a 5% annualized rate.

This example is an interesting corollary to the assertion that growth is critical to investment returns. I am a big believer in reflexivity when it comes to investing, and everyone knows that everyone knows that growth is important. Thus, growth is expensive.

I am not making an argument for buying cheapness per se, but where expectations are extraordinarily low, even a moderation in a declining trend can constitute a ‘growth surprise’.

Of course we can’t buy Altria 5 years ago, but we can buy something better.

Source: Cayucos Capital

Molson Coors is the junior partner in the US beer duopoly with Anheuser Busch. Through its ownership of Miller Coors, Molson commands a quarter of the US beer market by volume, with Anheuser Busch taking another 1/3.

I’ll say that again, one quarter of the US beer market – 10 billion pints (or 12.1bn 16oz servings) annually - and available for $7.7bn. That wouldn’t even build you a 1GW data center, is less than 1.5x what it cost to build the SoFi Stadium hosting the US’s opening World Cup match, the equivalent of just 30 Boeing 787 Dreamliners. I know I’d rather own a quarter of the US beer industry than 30 jumbo jets!

Its no secret that the US beer market has been declining in volume terms for many years. Interestingly the impact of craft beer has not been meaningful, with craft brands in aggregate claiming 13% (the same as 2019). The main reason for the industry-wide decline is changing consumer behavior, particularly among younger age cohorts who seemingly drink less alcohol. This trend is compounded by higher marijuana consumption in the US, and more recently the rise of GLP-1s.

That said, humans have been drinking beer for thousands of years so I don’t believe this is trending to zero. My view is that there is a cyclical fashion element to alcohol consumption. In the same way that high waisted pants and Reebok sneakers cycle in and out of fashion, the drink of choice cycles between beer, wine and spirits. Ordering a beer at a cocktail bar may be analogous to walking in in flared jeans today but it will not always be so.

Capital Allocation

The other key aspect to value (other than growth), is capital allocation. It is this component that often catches out value investors and turns ostensible ‘value’ into a value trap. A company may be very cheap relative to historic cashflows, but if those cashflows are funneled back into a business in terminal decline the outcome will not be pretty.

I tend to believe that professional management teams are significantly misaligned when it comes to a shrinking core franchise – their options packages lead them to swing for the fences with drastic moves like transformational M&A, doubling down on reinvesting in a fading business etc. The last thing they want to do is shrink the business, even if this is the best thing to do on a per share basis because, empirically, executives of smaller companies get paid less.

This is where Molson Coors has an advantage relative to Altria because it has a long term owner, or more accurately two.

A Brief History

The Coors side of the business dates back to 1873 when German immigrants Adolph Coors and Jacob Schueler bought a Pilsner recipe from a Czech acquaintance and set up a brewery in Golden, Colorado which remains open and is today the largest single-site brewery in the world.

Source: Molson Coors

And sorry, just to labor the point even further, the value of residential real estate in Golden, Colorado – a city of 20,000 people – is approximately $7bn, i.e. almost equivalent to a company that commands a quarter of the US beer industry!

The Coors family owns 15% of the company today, and effectively control it through A shares. These have broader voting powers than the more restrictive B shares that minority investors can own.

The Molson side dates back even further to Montreal in 1786. Recent English arrival John Molson began working at the Thomas Loyd brewery in Montreal. Loyd neglected to pay his workers who sued him, resulting in the brewery being put up for auction by his creditors. John Molson saw the growing demand for beer driven in part by the boatloads of his compatriots arriving. He seized the opportunity and, thanks to an inheritance from his parents, was able to acquire the brewery he’d begun working at as a 20 year old just a year prior. The Molson family own 3% via A and B shares.

The two sides came together in a 2005 merger. Today there are two Coors on the board, including the Chairman David, and 3 Molsons, including Vice Chair Geoff. The Coors side are the fifth generation of the family to be involved in the company, while the Molsons are 7th generation, one of the oldest family run businesses in North America.

The history of the consolidation of the global brewing industry has been told elsewhere, most colorfully in Dream Big which charts the journey of 3 Brazilian bankers, Jorge Paulo Lehman, Carlos Sicupira and Marcello Telles, who first dominated the beer industry in their home market before using these cashflows to take over a sleepy business via aggressive acquisitions of much larger companies. Most notably they pounced on Interbrew, the maker of Stella Artois in 2004, followed by the even more daring hostile takeover of Anheuser Busch, maker of Budweiser, in 2008. Finally the coup de grace was the $107bn 2016 merger with SAB Miller, the world’s second largest brewer.

One of the key sticking points of this 2016 merger was SAB’s 58% stake in Miller Coors which controlled a quarter of the US beer market, and clearly couldn’t be allowed to fall into the hands of Budweiser, which itself controlled another 1/3. Hence SAB sold the stake to their partner Molson Coors in a $12bn transaction, also consummated in 2016.

It is clear with hindsight that Molson massively overpaid for this asset, paying roughly 20x earnings for a business with declining volumes. The total enterprise value today of the group is $7.7bn plus $6bn debt = $13bn, i.e. scarcely half of what they paid for the US business alone. Molson took a $3.6bn writedown on the asset in 2025, plus $845m in 2022.

The company does have an ex-US & Canada business, including a strong position in the UK. This division accounts for a little over 1/5th of sales, and is marginally profitable so I won’t dwell on it.

Since the Miller deal, the group has spent much of the past decade paying down the debt they took on to complete the transaction, which peaked at $11.5bn, and is down to $6bn today, about 4.5x FCF ex interest. The remaining debt is very long term and relatively cheap, including a 2046 $1.8bn bond paying 4.2% and a $1.1bn 2042 bond (5%), as well as a 2036 $1bn note (5.5%).

The company just refinanced debt set to maturity next month and so now has no maturities before 2031. This frees the company to spend its free cashflow on buybacks and dividends which it has been aggressively doing in recent years. In the last twelve months, Coors spent $760m on buybacks and a further $370m on dividends, which equates to a dividend yield of 5% and a buyback yield of 10.5%.

If you are buying back and cancelling shares outstanding at a runrate of over 10% of the company annually, it is really not very hard to grow per share revenue and profit, even if the business is shrinking on a unit volume basis.

Source: company filings; consensus estimates from Capital IQ; volume estimates from Alphasense

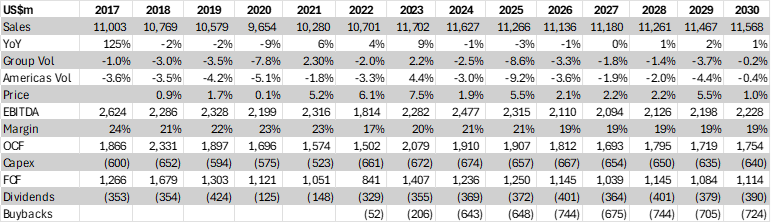

You can see that volumes have been declining for some time by a little under 2% annually, but thanks to price growth that has translated into a couple of points of sales growth. The consensus expectation is for more of the same. In 2025 Molson terminated some contract brewing relationships (they were brewing Asahi and other brands in the US) which according to the company cost them 3% of volume decline. I haven’t adjusted for this in the above table. Regardless, 2025 was a tough year which has instilled fears that beer volume decline is accelerating. Notably Anheuser Busch did -3% volume in its North America division in 2025, so I think there is also an element of competitive back and forth with Coors ceding some share more recently.

But in any case, the key point is that, even with volume decline, if you are buying back 10% of the company annually, something that is eminently sustainable at this valuation, double digit per share sales growth is quite plausible. And it is our share of sales/ profits/ cashflows that matters. Even if we use very bleak assumptions of 4% volume decline and 2% pricing growth, with a share count declining at 10% a year, mathematically that equates to almost 9% growth in sales per share. And the beauty of buyback math is that the more miserable the market is about the company’s prospects the more accretive buybacks can be.

If not now, when?

As to timing, I say this slightly in jest but there is in this case a genuine ‘World Cup effect’ – Jeffries estimates that 1bn additional pints will be consumed on account of the soccer World Cup globally(!) so companies like Molson will see a bump in their numbers in the current and next quarter, particularly as the US & Canada are host nations. And Scotland is participating for goodness sake!

Coors Light is rolling out the Tallerboy and you’re bearish??

It is perhaps notable that after years of dismal performance consumer staple names have seemingly finally begun to catch a bid. At the risk of being incredibly short term, at Wednesday’s close the XLK (Technology ETF) was down 8% over the prior 5 trading days, while Molson is up 5%, and other beaten down names like Campbell’s Soup is up 6%, while Clorox (maker of bleach) is up 10%, with each bouncing off decadal lows. So who knows, we could be witnessing a rotation in the market.

20 Year Share Price Chart

The stock is basically where it was 20 years ago!

Finally there has been a little bit of buying from both sides of the family. Andrew Molson bought nearly $100k of stock in March @ $46.70, and a further $350k in Nov 2025 at a similar price. Chairman David Coors also bought $100k in Nov 2025. I don’t want to overly emphasize these purchases because the dollar amounts pale in comparison to the dividends the families receive from the company ($68m in 2025) but these individuals already have a large economic and also reputational exposure to the stock so it is always interesting to me when insiders decide to put their hands into their pockets to buy stock. These are open market purchases not stock grants from the company.

For full disclosure, Vice Chair Geoff Molson sold just over $50k in May @ $42.50 and $75k the year prior (@ $56). I don’t find insider sales to have as much signal value as buys but the amounts are quite curious for a man with a net worth north of $1bn (primarily related to his majority stake in the NHL franchise the Montreal Canadiens). $50k presumably pays for a modest weekend in Geoff’s world!

Here is Geoff Molson describing his net worth

Conclusion

Brewing is one of the oldest businesses in the world and so I wouldn’t bet on complete obsolescence. However, especially given the debt here, there is a risk of a death spiral where volume decline accelerates, leading to operational deleveraging and collapsing cashflows no longer able to support the debt load.

In a fragmented market this dynamic risks creating a prisoners dilemma scenario where all players are tempted to cut prices in order to grab a greater share of volume and maintain operating leverage, however operating in a duopoly mitigates this risk.

Also the long tenure of debt means that the company can pause buybacks and reduce debt quite quickly even if cashflows disappoint.

The two families are, slowly, taking the business private, one buyback at a time. But perhaps they will eventually decide that they are not the right owners of the business and succumb to the consolidation that has swept the global beer industry. There are a number of obvious suitors or merger partners, particularly global brewers like Heineken or Asahi which lack a meaningful presence in North America. Even firmly family controlled companies can potentially be put in play, as we have seen recently with Brown Forman, which has a similar ownership structure. This should provide a floor to the stock.

Despite the growth challenges, this is a business that millions of loyal customers buy products from every day. It can’t be disintermediated by the internet, nor disrupted by AI (I don’t think?!). So I thought it ought to command a rating greater than 7x FCF. Even a modest rerating to 10x FCF with buybacks would give us a per share annualized return of 17% over 5 years using our previous assumptions of 4% volume decline, 2% price growth and flat margins. BUY!

This article is purely for informational and entertainment purposes and should not be construed as investment advice. Please consult a financial advisor before making any investment decisions.

Please also assume that I own and intend to trade any stocks discussed before and after dissemination of this report.

Has there been a brewery in last ~10yrs that has been an exception to the downward rule ?

Mr Molson might be describing his significant net worth but if he and his forebears were competent they'd own way more than 3% of the company ?? (plus 15% Coors side, and this is after buybacks too). It's not like they need space travel or AI levels of other-people's-money...

If share price did go up they could/should buy back bonds as alternative and accretive use of money

Has there been a brewery in last ~10yrs that has been an exception to the downward rule ?

Mr Molson might be describing his significant net worth but if he and his forebears were competent they'd own way more than 3% of the company ?? (plus 15% Coors side, and this is after buybacks too). It's not like they need space travel or AI levels of other-people's-money...

If share price did go up they could/should buy back bonds as alternative and accretive use of money

Thanks!!

CD