Jardine Matheson

A perennial value stock finally has a catalyst, and we’re paid to wait. $J36.SI $JMHLY

Jardine Matheson is a diversified Asian conglomerate owning everything from Mandarin Oriental hotels to 7-Eleven stores. It also has one of the most fascinating histories of any public company on the planet.

Named after two Scottish traders who made a fortune in the early 1800s smuggling opium from British controlled India into China. The Chinese went to war with the British in order to end this trade and the resultant treaty in 1842 led to the ceding of Hong Kong island to Britain.

However wanting to add another ‘sin’ trade to their repertoire, they became arms dealers, supplying then-rebel forces who led the Meiji Restoration that returned imperial rule in Japan in 1868.

Deciding to settle down in the newly established colony of Hong Kong, William Jardine and James Matheson used their profits to buy land in the territory and build an Asian trading empire there. Jardine’s niece married Thomas Keswick and their son William ran the group from 1874 to 1886. The fifth generation of Keswicks still control the company today with a 33% stake.

The Keswicks and Jardine Matheson, hereafter JM, are responsible for building much of modern day Hong Kong. In 1979/80 the group acquired a 40% stake in Hong Kong Land, at the time the world’s largest property company according to the New York Times. Shortly after, Hong Kong Land won a bidding war for the last major site available for development in Central Hong Kong, paying over $500m for what would become Exchange Square. The timing couldn’t have been worse as a property slump ensued and office rents halved. This plunged both companies into crisis and potential acquirers began to circle.

In order to ward off suitors, and wary of the recently signed agreement to hand Hong Kong back into Chinese oversight in 1997, the JM group took the drastic decision to move their companies’ incorporation to Bermuda. As one of the only major groups to incorporate there, JM allegedly had a significant hand in writing the corporate governance code, making it extremely difficult to execute a hostile takeover. Even so, the group decided to create a convoluted crossholding structure to make themselves even more impervious to outside forces.

Protected from takeover, the Keswicks were slowly able to put the business on firmer footing by selling off assets and reducing their debts, eventually putting themselves in a position to grow again, acquiring a prime asset in Indonesia in the wake of the Asian Financial Crisis of 1997. But the cross holding structure remained and the stock market was thus largely disinterested in the group, despite a disconnect between the market cap of JM and the value of the underlying assets.

However this has begun to change. Ben Keswick, great-great-great-grandson of Thomas Keswick took over as Executive Chairman in 2019. In 2021 he was finally able to unwind the cross holding structure, fully acquiring sister company Jardine Strategic.

As a family member taking over, there is only so much you can do without stepping on toes. However his Uncle Sir Henry Keswick, who had long been Chairman of the group between 1972 and 2018, and latterly had an (in theory) honorary title of Chairman Emeritus, died in November 2024.

Then the following month Ben’s cousin Percy (Keswick) Weatherall stepped down from the board. The 68 year old had worked in the group since 1976 and been CEO for much of the 2000s.

German physicist Max Planck is paraphrased as saying that science progresses one funeral at a time, and sometimes reform of family companies is similar. It appears that Ben has consolidated his control and now has a freer rein to overhaul the group.

John Witt, a 30 year lifer is stepping down as CEO and rather than being replaced by a trusted insider, his successor will be Lincoln Pan, a partner of leading private equity firm, PAG.

In a similar vein, the new head of China comes from another major PE firm, TPG, and his number 2 was Head of Asia Pacific M&A for Bank of America. Again the latest appointments to the board are Ming Lu, Executive Chair of Asia Pacific for KKR, and Janine Feng, an MD of Carlyle.

I don’t mean to suggest that private equity is some kind of panacea. In fact far from it, my general view is that PE often provides limited value beyond financial engineering. But in this case, these appointments, in contrast to a history of promoting from within and entrusting long term veterans, are indicative of a desire for radical change. Indeed, though Ben Keswick has never granted a media interview, an insider was quoted by the Financial Times, in 2021, as “trying to modernize the business at an urgent pace.” The other reason you put PE execs and bankers in charge is because you will be facing off against investment bankers on the other side of the table in asset sale talks.

No doubt the group will have had to pay up to lure these executives away from their PE roles, and the company notes it has adopted a “new incentive framework [to] better align performance of leadership teams with creation of long-term shareholder value.”

But the evidence of change is not just in terms of personnel. Under Ben Keswick there have been a number of divestments which I will elaborate on below.

So what is Jardine Matheson?

The group is an extremely complex sprawling conglomerate with at least 12 publicly listed entities so I could easily dive down any number of rabbit holes, but for the sake of understanding I will attempt to simplify greatly.

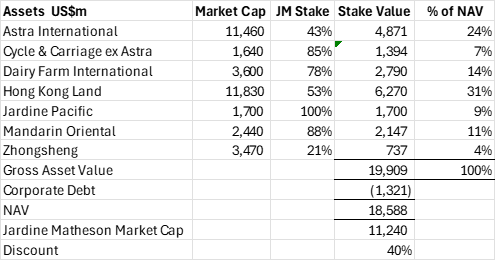

Firstly, here is the Net Asset Value (NAV):

So you have 7 main businesses, of which 6 are publicly listed – 5 in Singapore, and Zhongsheng in Hong Kong - and therefore the market value is explicit. Then there is Jardine Pacific which is 100% owned but pays pretty consistent dividends which I value at 10x (10% dividend yield). So on this basis you have $18.6bn of assets net of debt, which you can buy for $11.2bn i.e. a 40% discount.

I will briefly summarize the respective businesses – let’s see if I can do it in two sentences for each:

Astra is a giant Indonesian conglomerate involved in construction equipment, mining and car and motorbike dealerships. They sell (and finance) over half of the new cars purchased in Indonesia - a country of 250m people - as well as 80% of the motorbikes through long term relationships with Toyota and Honda among others.

Cycle & Carriage in addition to being the direct owner of Astra, C&C owns stakes in a number of Vietnamese public companies including the leading dairy business and a car dealership group. Also distributes Mercedes Benz and other brands in Singapore and Malaysia.

Dairy Farm - despite the name - operates over 3,000 7-Eleven stores, as well as drug stores and grocery stores in Hong Kong, South China & Singapore. They are also the Ikea franchisee in a number of countries as well as for Starbucks in Hong Kong.

Hong Kong Land is a prime real estate owner in Hong Kong and Singapore, which also does residential and commercial property development in China and other Asian countries.

Jardine Pacific is itself a mini-conglomerate, consisting of construction businesses, over 1,000 franchised KFC & Pizza Hut restaurants as well as a joint venture with Schindler to manufacture and service elevators all across Asia.

Mandarin Oriental is the iconic hotel brand. They have 40 hotels globally.

Zhongsheng is the leading independent car dealer in China, retailing primarily Mercedes, Toyota and BMW.

But to simplify further, the business is really Hong Kong Land, Astra and Other.

Hong Kong Land (HKL)

I will start here, firstly because it’s the largest chunk of the NAV, but also because this is where there is a lot of scope to unlock value.

In keeping with recent changes, there is a new CEO, Michael Smith. He was a senior executive of the real estate investing business of Temasek, one of the largest investors in Asia, and before that headed South East Asian Investment Banking for Goldman. By contrast, his predecessor was a company lifer who moonlighted as a Professor in his spare time.

If you go by Jardine’s numbers the value of HKL is not the $12bn the market assigns to it but over $30bn. Now this is using a rather aggressive sounding 3% cap rate (Net Operating Income/ Market Value) for their prime Hong Kong and Singapore office properties. If I simply take the rental income and divide by the market cap plus net debt that gives me a market assigned cap rate of over 8%. I’m not sure what is the right number, but 3% seems too low, and 8% likely too high.

However I don’t want to dwell too much on what is an appropriate cap rate because cutting the market implied rate by 1 or 2% doesn’t make for a very compelling investment case.

More interestingly HKL has announced $10bn of asset sales, i.e. almost all of the current market cap. Most of this will come from the gradual wind down of residential developments in Mainland China, as well as the disposal of Mainland shopping malls.

The company has also mooted putting some of its assets into a REIT (Real Estate Investment Trust) or finding some other way to bring in 3rd party capital, which either way would amount to a partial sale of assets, unlocking capital.

And most recently, in April 2025, the group announced it will sell the top 9 floors of its flagship One Exchange Square office tower to the Hong Kong stock exchange for $800m, and will use part of the proceeds to buy back its own stock.

This is notable not just because it is an asset disposal realizing value, but also because Exchange Square is the company’s crown jewel, the asset they nearly lost the company betting on in the 1980s. The fact they are willing to sell it is indicative that there are no sacred cows and that the group is serious about unlocking value. One Exchange Square has a further 41 floors of office space which JM continue to own as well as a further 51 floors across the road at tower Two. By my calculations this transaction seems to imply a 4% cap rate.

Astra International

As a conglomerate within a conglomerate – the largest company in Indonesia by sales – Astra moves to its own beat. Hence, as far as I’m aware nothing has been announced specifically relating to restructuring or asset disposals.

However, there are plenty of levers to unlock value. Astra trades for less than its tangible book value despite consistently generating a high teens ROE (return on equity), and a P/E of less than 6x trailing earnings, which as you can see below is historically low:

Also the group pays substantial dividends up to Jardine Matheson, paying $1.2bn or over 10% of the current market cap out to shareholders in 2024. So that is certainly one mechanism to unlock value for JM.

Other

Within this ragtag of ‘Other’ assets, Ben Keswick has in fact taken a number of steps to simplify things already. These include:

o 2023: sold their UK car dealership business with $2bn of sales

o 2023: Dairy Farm sold its Malaysian grocery business

o 2023: sold their 28% stake in packaging company Greatview Aseptic for $130m.

o Jan 2024: sold their half of the baggage handling operation at Hong Kong airport.

o Apr 2024: Dairy Farm divested Hero Supermarkets, its Indonesian grocery chain

o Aug 2024: Cycle & Carriage sold their minority stake in Siam City Cement

o Oct 2024: Jardine Schindler sold its Taiwanese business.

o 2024: JM increased its stake in Cycle & Carriage by nearly 7% to 85%. It seems likely they will buyout minorities removing a layer of complexity.

o Feb 2025: Dairy Farm sold its 30% stake in Chinese grocer Yonghui Supermarkets for $900m.

o Mar 2025: Dairy Farm announced the sale of its Singapore grocery store business for $125m.

In association with Dairy Farm’s sales of businesses in Singapore, Malaysia and Indonesia the group disposed of over $250m of property assets in 2023-24. With these disposals and the Yonghui cash the Dairy Farm balance sheet will be considerably net cash and with a 22% free float they could easily take this private also. There’s also a saleable stake in a Filipino retailer with a market value of $200m. Incidentally the CEO who has been tasked with executing this strategy at Dairy Farm is a former CEO of Wal-Mart Asia who immediately prior to this had senior roles at UPS International, a business that runs a very asset light model.

JM also increased its stake in Mandarin Oriental in 2024 by nearly 8% (to 88%) and this could be another buyout target. In addition, Mandarin Oriental has established a “new strategy to accelerate brand led management business.” In plain English this means rather than owning the expensive real estate underlying a luxury hotels business they are trying to shift to a model where they have a management contract to operate hotels owned by a 3rd party. They have already signed 8 such contracts (relative to a portfolio of 40 hotels which they want to double via this new strategy).

Moreover, two flagship hotels have been sold in recent years including Paris in 2024 for $225m (while retaining a 50 year management agreement) and Washington DC in 2022 for $140m (which they will no longer operate).

I believe there is a lot more to come - Lincoln Pan, the new private equity CEO hasn’t even started yet. He arrives 1st December. Per Jardine’s latest analyst presentation, my emphasis added: “5 year & 10 year TSR [total shareholder return] disappointing. Strong focus on evolving the portfolio through disciplined capital allocation to ensure future delivery of superior 5 year TSR”.

The Numbers

The financial statements of conglomerates are a mess because where they own more than 50% of an entity they consolidate this entity into the group accounts. In JM’s case this is further complicated by the fact that Astra has a fairly large financing business (effectively a bank financing the purchases of cars and motorbikes).

So I won’t present the full financials here to avoid confusion. Here is JM’s share of net profit of the group companies:

I have adjusted these numbers to include the stakes held by Jardine Strategic which was acquired in 2021. You can see that despite lots of moving parts the diversity of the group means that the overall earnings are fairly stable, notwithstanding a disrupted 2020. You can also see that a number of businesses have struggled to recover to their pre-COVID glories.

JM has been buying back its stock since 2017, although these purchases have been modest and have reduced in recent years. The company has promised more in the future however.

Risks

The first risk is one of capital allocation. The group could very easily take the proceeds of all these asset disposals and restructurings and plow them back into new assets further adding to the complexity of the group. For example just in advance of all of the disposals detailed above, in early 2020, the group spent $4.4bn buying a massive plot of land for development in Shanghai. The timing could hardly have been worse coming weeks before the emergence of Covid and the Chinese property implosion. Something similar is certainly possible although would be a complete U-turn from the recent public statements and actions of the group. We are also, at least theoretically, well aligned with the Keswick family in so far as they are the largest shareholder with 32% of the shares.

Secondly, as above, a large part of the net asset value is Hong Kong property. If ultimately Hong Kong’s future is as just another Chinese city as opposed to a critical conduit between China and the West then there is a lot of downside to the value of Hong Kong Land’s assets. A top law firm or bank no longer needs to rent offices in Hong Kong but instead has a choice of any number of Chinese cities from Shenzhen to Shanghai to Beijing so rents will come down. This has already been happening to some extent with Hong Kong office rents falling in each of the last 4 years, and flat in 2020. Overall office rents are down 40% since 2019 according to CBRE. However rents remain 5-10x higher than Shanghai for example, so there is room for them to come down further.

Thirdly as with any value trap (a cheap stock that stays cheap or worse, gets cheaper), the stock could continue to be priced at a discount to its underlying assets. I first wrote about the group in 2012 (my recommendation was sell!) and there was a substantial discount back then. Asset disposals, particularly the residential real estate business they are winding in China, could take some time to materialize. Even in taking several more steps to simplify the group it will no doubt remain a complex conglomerate. And when a stock is complicated, market participants will often label it too hard and move on to something else that they can more easily build a financial model for. There are no points for degree of difficulty in this business after all.

That said I try to own companies where I can buy future cashflows cheaply regardless of what the market thinks of them. In this case, at the current entry level we are getting a 5% dividend yield which has scope to increase: JM is only passing on about 1/3 of the dividends it receives from its underlying companies. And I expect this to be augmented by a combination of special dividends, buybacks and increasing stakes in the underlying businesses (which leads to higher future cashflows and dividends). The critical point to avoid getting stuck in a value trap (I perhaps need to write an article on these) is that there is a catalyst for change, and here I think there is ample evidence for this change.

Valuation

I am reluctant to put a valuation here. I could easily ascribe an arbitrary discount to NAV of say 20%, but this would be a number plucked out of thin air. The whole point is that I expect to see continued corporate transactions, and that these will unlock value and be returned to shareholders in some form be it dividends, buybacks, reinvestment in existing businesses and/or a narrowing of the discount.

In sum this future corporate activity could exceed the current market cap, leaving a collection of assets again worth the current market cap for 100% upside over 5 years. BUY.

Thanks for reading! Please think of one person that might find this article and share it with them - let’s make Asian conglomerates go viral!

Disclaimer

This article is purely for informational and entertainment purposes and should not be construed as investment advice. Please consult a financial advisor before making any investment decisions.

Please also assume that I own and intend to trade any stocks discussed before and after dissemination of this report.

Good summary of the situation. I own both Mandarin and JM in my fund albeit JM is larger. I agree completely with your comments on the importance of the change in approach. Will be interesting to see how the next couple of years play out

On the last call I was Witt must have mentioned shareholder value a dozen or so times. If JM are getting serious now they certainly have a lot of levers to create value. A large buyback would be a great sign the empire building of the past is no more.