Cosan

The world's largest sugar producer. $CSAN

This is not a company I would typically write up. It’s highly leveraged, highly complex and the core business is a low quality, price-taking commodity producer. However enough has changed to pique my interest that an inflection could be approaching. And when you have all of those ingredients I have chalked up in the negative column, a positive inflection can lead to a very powerful share price move.

History

Sugar is a product you probably don’t spend much time thinking about, but it is ubiquitous, sitting in almost every kitchen around the world, not to mention our favorite sweet treats. The world consumes about 180m metric tons a year of the white stuff, which works out to 45kg per person in North America and about half that in developing nations. US per capita use has fallen by 1/3 since 1970 due to health trends, which has been more than compensated by growth driven by rising wealth in poorer countries.

Brazil is the world’s powerhouse in sugar production, responsible for about ¼ of global supply.

The roots of Cosan go back to 1980 when Brazilian entrepreneur Rubens Ometto took over a single sugar mill in Sao Paulo state that his grandparents had founded 50 years prior. From this beachhead he was able to aggressively consolidate the Brazilian sugar milling industry, eventually becoming the largest producer in the world. Ometto today owns 21% of the company.

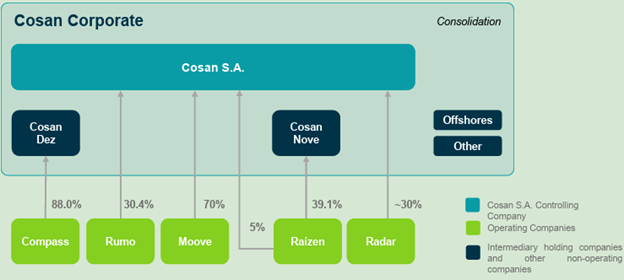

Sugar milling is a highly commoditized, capital intensive, cyclical business and so over time, Ometto has diversified the group into a broad conglomerate, expanding into ethanol (which is used as a fuel in cars), lubricants (Moove), gas stations (in JV with Shell), railways (Rumo), natural gas pipelines (Compass) and agricultural land ownership (Radar).

Here’s how they present the corporate maze:

There is a great deal of debt in this structure, at Holdco level, at Cosan Nove & Dez (9 & 10), and particularly at Raizen, as we will get into.

All this complexity (and leverage) has not paid off, with an abysmal share price performance since the IPO back in 2005. The below chart is in Reals but would look far, far worse in $ terms:

Many Ways to Win

All of the above would typically be enough for me to quickly pass. However there are a number of very interesting catalysts at play.

Catalyst #1: higher sugar prices

The Iran conflict has flipped the board, drastically changing many macroeconomic variables. Unless you live under a rock you will have seen plenty of analyses laying out the magnitude of oil and other commodities unable to transit the Strait of Hormuz

But As Javier Blas recently pointed out, there are two elements to a crisis, the size of the disruption and the duration. It is the latter which is the big unknown. For now, per the CME website if you want Brent crude in December this year, the current quoted price is $80 a barrel, well below the spot price of $110 as of this writing, implying that the disruption in the oil market at least will be relatively short-lived.

There are two reasons why I like the sugar angle. The first is that sugar has been going through a long term down cycle as you can see from the below price chart (which shows the cost of 100lbs of raw sugar for delivery next month):

Indeed Cosan’s sugar & ethanol business Raizen - the largest sugar mill in the world - was loss making last year.

The second is that disruptions to the Strait of Hormuz right now could cause significant longer term implications for sugar, regardless of whether the conflict is resolved.

Let me explain.

The most widely used fertilizer in the world is nitrogen in its various forms (primarily urea). Urea is made from ammonia which is produced via giant Haber-Bosch plants. These take nitrogen from the air and fuse it under very high heat and pressure with hydrogen. That hydrogen in almost all cases comes from natural gas (CH4).

Natural gas is quite hard to transport, requiring lots of infrastructure either to pipe it or to cool it and put it on LNG ships. Urea, being a solid at room temperature, is much easier to move around. Thus much of global urea production tends to be located in close proximity to cheap natural gas. Hence North America, Russia and in particular the Middle East.

The Middle East represents about 10-12% of global urea production, but well over 1/3 of global exports as major consumers like China, India & the USA produce much of what they consume. But of course the price of commodities is set at the margin and so Middle Eastern urea sets the global price. And it is not just that urea and its precursors are stuck behind the Strait, there has also been meaningful damage to production infrastructure which will take years to rebuild.

Brazil is particularly sensitive to global urea prices because it produces very little nitrogen fertilizer domestically, making it the world’s largest importer. Brazilian sugar growers, by far the largest producers in the world with around ¼ of the global market, buy the majority of their fertilizer in the southern hemisphere winter (May-August), which means imports into the country begin ramping up in the April to June period.

Due to the Iranian conflict, importers and farmers have been forced to make tough decisions. Brazilian urea prices rose 40% in March and are nearly 100% higher than a year prior, which combined with low sugar prices, means that many farmers will choose to reduce their use of fertilizers, resulting in lower yields when the crop is harvested in a year’s time.

But wait, there’s more!

In Brazil over 90% of vehicles sold are flex-fuel vehicles which means they can run on gasoline blended with ethanol, or even pure ethanol. Hence roughly half of Brazilian sugarcane is turned into ethanol to be sold in gas stations, but this proportion moves around depending on the oil price. So due to rising prices of crude and its derivatives, mills divert more of their output to ethanol, effectively reducing sugar milling capacity and thus leading to higher prices.

Catalyst #2: recapitalization and outside shareholders

A key part of my investing framework is to try to invest alongside aligned principals, and per the share price chart above, Rubens Ometto’s track record doesn’t exactly inspire confidence.

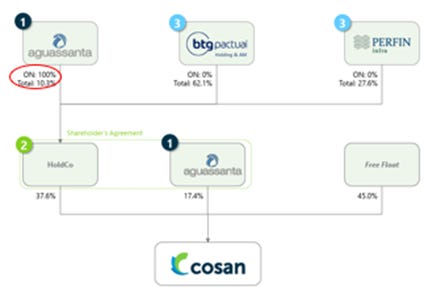

However, in September 2025, Cosan announced a large R10.5bn ($2bn) capital increase, substantially fixing the balance sheet. Not only that, but the rights issue was largely funded by two local asset management groups, Perfin and BTG.

I don’t know a lot about Perfin, but BTG and in particular its Chair, Andre Esteves are regarded as very shrewd investors. Esteves and his partners famously sold their bank to UBS in a $2.5bn deal in 2006 and then took advantage of the great financial crisis to buy it back from the by then beleaguered Swiss bank.

Today, Esteves has a personal net worth of $14bn per Forbes, making him one of the top 10 wealthiest people in Latin America. BTG put $1bn into the deal, gaining a 23% stake, with Esteves becoming Vice Chair (he has only ever served on one other non-BTG board before as far as I know).

What does give me pause though is that BTG and Perfin, who have agreed to lock up their shares for 4 years, have effectively handed over their voting rights to Ometto. He thus fully controls the Holdco, and thus Cosan. Moreover Ometto himself also personally put up R750m ($150m) of his own money into the deal and has secured the Chairmanship for the next 6 years (he’s 75). He’s therefore hardly retiring gracefully into the background.

That said, again, BTG are very shrewd investors and so they have surely thought carefully about how to secure their large investment. It is possible we are not well aligned with BTG here despite owning the same shares: they already have capital at risk with Cosan on the bank balance sheet and also will get a lot of investment banking work from Cosan. They are already the lead banker on the Compass IPO (see below).

Catalyst #3: asset sales

In addition to fixing the Cosan balance sheet with the capital raise, there have been rumors and in some cases concrete actions around disposals and simplification of the group. The most significant would be:

Compass – recently filed for an IPO of the 88% owned nat gas distribution company and is expected to raise $1bn.

Raizen Argentina (gas stations & refinery) reportedly up for sale. Cosan paid Shell $1.35m a station in a 2018 transaction. Arguably the investing environment is a lot better in Argentina now than 2018, but conservatively: 1,225 stations @ $1.35m each implies $1.7bn.

Moove – the 70% owned lubricants business is on the chopping block. This was slated for an IPO in the US in late 2024 but Cosan (and their minority partner CVC) failed to attain their intended valuation of $1.9bn. The company had a major fire in early 2025 which has complicated a sale.

Catalyst #4: Raizen recapitalization

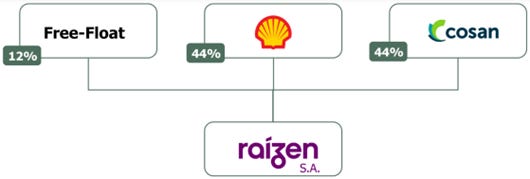

The sugar & ethanol exposure is held via a 44% stake in Raizen, a Brazilian listed entity (with no ADR). Raizen is a very large business, with $42bn of sales in 2025, though due to excessive leverage and operating losses in the past year, its market cap is just over $1bn.

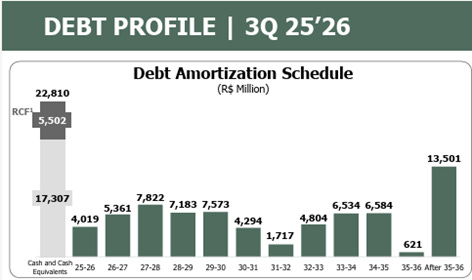

Raizen has over $10bn in debt as a result of heavy investments in recent years including a poorly timed acquisition of a sugar/ethanol rival in 2021. However, the company doesn’t have any immediate funding needs as the chart below illustrates:

Nor does the company have any leverage or debt service based covenants. That said, Raizen has apparently decided to preemptively address its unsustainable debt load and proceed with an out-of-court settlement with its creditors and now has 90 days to reach a court ratified plan. Under the plan, Cosan and its JV partner Shell will likely put equity in, with a portion of debt converting to equity and a plan of divestitures agreed. I see this as broadly positive for Raizen as the equity is already heavily discounted to reflect likely dilution.

And when you have a thin sliver of equity in a highly leveraged structure, a small improvement in the fundamentals driven by higher sugar prices can have a dramatic impact on equity value.

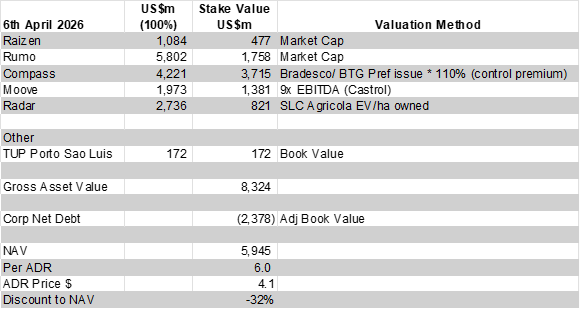

Sum of the Parts

Here is a simple valuation which takes the public market cap of the two listed subsidiaries, a recent capital raise at Compass, the recent disposal multiple of Castrol by BP and a peer valuation for the land business Radar.

Net debt accounts for the recent capital raise and is adjusted to include all liabilities at the intermediate Holdco level.

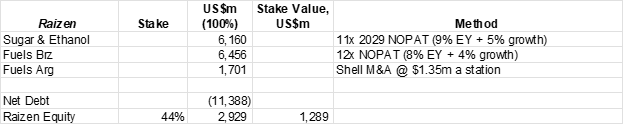

So you get a healthy discount to the parts, but as I have argued above the market could be materially undervaluing Raizen, the sugar and ethanol business. Below I have further broken down the parts of Raizen:

I have used very conservative assumptions here. For example, 12x NOPAT (net operating profit after tax) for the fuels business (gas stations) compares to listed peers that trade at 15x and 17x. And the sugar business is valued based on some work I did in January (i.e. before the Iran disruption) which assumed a very gentle recovery out of the sugar downturn and without the benefit of higher ethanol prices.

But even this modest assumptions add $800m to the Cosan NAV, or a further 20% upside to the current market cap.

The big unknown is the extent of dilution that will be required to recapitalize Raizen. With the market cap so small there is clearly a risk that dilution will have to be large to raise meaningful capital. For example, just to take debt down by 10% would imply doubling the share count.

What is somewhat reassuring is that the two major existing shareholders – Cosan and their JV partner Shell, who each own 44% - will most likely put up the bulk of the capital and are not incentivized to torch the existing equity. However I do prefer to be in the Cosan equity because to the extent this entity puts up capital at a very low price, this advantage accrues to Cosan shareholders at the expense of existing Raizen holders.

Again, Raizen has no pressing funding needs and higher sugar prices will help greatly.

Conclusion

I have tried to keep things pretty high level here. This is clearly a highly complex situation and there are multiple threads I could have pulled on. Feel free to message me if you want to discuss any aspect of the story I have glossed over.

Evidently this is quite a risky investment given the leverage at multiple layers in the structure and the low quality of the core sugar & ethanol business. However the various catalysts I have highlighted as well as the depressed point in the commodity cycle make this an interesting buy in my opinion.

I am also open to the idea that there are better ways to gain exposure to protracted disruption in the Middle East (again please message me!). Indeed I own a number of these and may well write up more in time.

Disclaimer

This article is purely for informational and entertainment purposes and should not be construed as investment advice. Please consult a financial advisor before making any investment decisions.

Please also assume that I own and intend to trade any stocks discussed before and after dissemination of this report.

The layered leverage is the honest risk here — you're not buying sugar exposure, you're buying a thin equity sliver in a highly leveraged conglomerate where the upside is dramatic but so is the dilution risk at Raizen. The fertilizer-to-yield-to-sugar-price chain is the most underappreciated catalyst in the write-up, because it plays out over 12-18 months regardless of how quickly the Strait reopens. BTG's involvement is the signal worth watching — Esteves doesn't put $1bn into deals he hasn't stress-tested.

Andre "jailbird" Esteves ?

I know probably more differences than similarities but... doesn't the Wilmar guy show everyone how you really turn a few plants and some plant-squashing machines into billions of dollars of equity? Wonder if the truly successful farmer types in Brasil are not listed?

Merci !