An Update on Rightmove

$RMV.L $RTMVY

My apologies for not publishing for a while. I have been very busy with personal matters, not to mention the day to day market moves taking up plenty of time and attention!

I wanted to write an update on Rightmove, the UK property portal, since my May 2025 note given it is the worst performing of my recommendations. In fact, Rightmove and Hemnet, another property portal, are the only profiled stocks that have lost money since time of writing. And boy has Rightmove lost money, the $ line is down 45%. I wrote of Rightmove at the time that it was “one of the best businesses ever conceived” and with hindsight I was guilty of overpaying for quality. Fortunately this is an error I rarely commit.

At the time of the report the stock was trading on 26x forward earnings, very much in line with the 20 year average of 25x. Since then the stock has traded down to 14x forward earnings per Capital IQ, which is the lowest rating Rightmove has commanded outside of the GFC (Giant Effing Crisis).

Forward Earnings from Capital IQ:

What then is the ‘correct’ multiple for the company. At the risk of sending the class to sleep, and with the caveat that I am a firm believer in the adage ‘better to be roughly right than precisely wrong’, I will introduce some algebra to exemplify how I approach valuation.

Perhaps the simplest way to value a company is based on the Gordon Growth Model which states:

In other words, price is next year’s dividend (D1) divided by required rate of return (r), minus growth (g).

However it doesn’t make sense to penalize a company for using earnings to reinvest in the business rather than paying it out to shareholders as dividends. If you own a company outright, there is in theory no difference between a dollar of profit retained in the business and a dollar dividended out. In fact the latter is usually subject to higher rates of taxation, so the former is arguably more valuable.

So we can substitute out D for E (earnings), to get:

P = E1 / (r-g)

So far so straightforward. The problem then becomes, what is r and what is g.

The way I like to think about r is that the long term (200 year) data shows returns from the US stock market are 6-7% real (i.e. after deducting inflation). Add in inflation of 2-3% and you get to a long term average nominal return of 8-10% (pretty pedestrian eh!, if only the Reddit crowd knew). This feels like a good starting point for a required return to own equities: you can add a premium for a stock that you perceive to be more risky in various ways, and in rare cases accept a slightly lower return for a stock where one perceives a very high degree of certainty of future cashflows.

Then to growth. One of the many things I have learned (the hard way) is that growth always matters. Even if you’ve found a ‘dirt cheap’ stock on 3x P/E, if cashflows are shrinking rapidly you are highly likely to lose money. Growth is thus a core component of value.

Anyway, the important point here is that growth has a very specific meaning, it refers not to growth in the next twelve months but growth in perpetuity. And in the long run everything trends towards GDP growth: mathematically anything that outgrows the economy in the fullness of time becomes the economy. So beware of being anchored to recent growth over short periods.

Over the past decade UK nominal GDP grew at just under 5%. If my required return is 10% then I can derive a fair P/E multiple of 20x:

P = E/ (r-g) => P/E = 1/(r-g) => P/E = 1/(10%-5%) => P/E= 20x

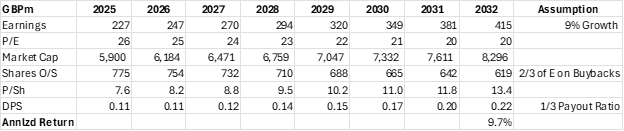

Stated differently, if Rightmove is ex-growth (beyond the expansion of the nominal economy) I think it should be worth 20x P/E. Based on a very simplistic model below, paying 26x implies (or implied) Rightmove continuing to grow at above terminal growth (9% pa) out to 7 years or 2032.

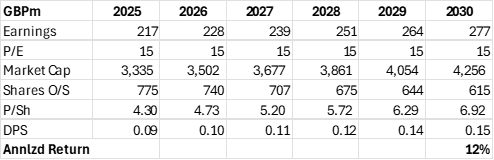

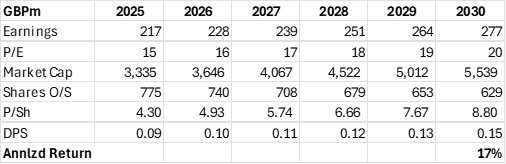

And this is where the market’s perception has changed drastically in the past 12 months. The market has seemingly brought forward terminal growth and is arguably even pricing for Rightmove’s decline/ stagnation. Because if Rightmove does indeed grow at 5% nominal over the next 5 years, shareholder returns would be 17% annualized with a rerating to 20x P/E, or 12% without.

No rerating:

Rerating to 20x P/E:

AI Loser?

This is where the quantitative meets the qualitative. In 2025 Rightmove grew sales by 9% -right in line with their guidance (and earnings by 12%). The company is guiding for exactly the same revenue growth in 2026 (8-10%) although they expect some contraction in margin due to AI-related investment, resulting in EPS growth of at least 5%. None of the (admittedly backward looking) data -from property transactions, property prices, wage growth or mortgage rates – point to an imminent slowdown.

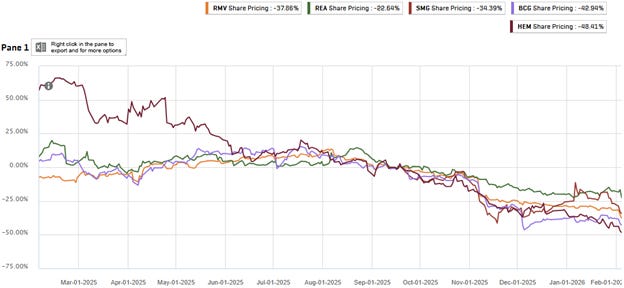

However the market seems to be pricing the whole global sector as a prospective AI loser with Rightmove down 38% in the past year vs REA 23%, Swiss Marketplace Group 34%, Baltic Classifieds 43% and Hemnet 48%:

I have learnt (again the hard way) that it is generally a bad idea to ignore what the market wisdom is telling you. However the perceived threat to these businesses is almost entirely in the future, so it is very difficult to substantiate these fears with hard evidence.

So I will start with what we can quantify thus far and expand to speculate about the future.

The first perceived risk I talked about in my Hemnet note. In that note, I wrote “in November, UK peer Rightmove announced that they would invest £60m ($79m) over 3 years to enhance their AI tools and the stock fell by over £1bn”.

That decline has expanded to more like £1.6bn today. Rightmove has since elaborated on that investment, saying that while revenue is expected to expand by 8-10% in 2026, EBIT will grow by just 3-5% (which actually implies slightly less than a £20m investment next year), with buybacks beefing that up to 5%+.

Clearly this relatively minor, possibly one-off, investment is not sufficient to account for such a decline in market value. (In fact if you were to capitalize the investment you would get an 80x multiple in terms of lost market value/ annual investment).

Hence the much more significant risk is the longer term disruptive threat from AI. I have tried my best to be imaginative about this threat and what I have come up with is a future where Chat GPT or equivalent is able to scrape the websites of all the real estate agencies, amalgamate all of that data and present that to the consumer in a user-friendly format, effectively cutting out Rightmove.

This is certainly possible, and the sheer amount of money that the likes of Chat GPT and Anthropic are raising is a massive incentive to go after any and all profit pools they can fathom.

However there are several reasons to be doubtful of this scenario:

Firstly Rightmove does all of the above for a total all-in operating expense of £137m ($185m). That is to say, Rightmove provides its service highly efficiently, and AI will likely help the company to reduce costs further. Their 2024 annual report stated the company had slightly below 900 employees. While the LLMs are certainly not focused on profits today, it is not clear they could do what Rightmove does at materially lower cost.

Secondly, data. The company claims to have 4Petabytes of data (a petabyte is 1m gigabytes), with the CEO stating on the recent earnings call: “we estimate that over 90% of our data is proprietary. This data is not available anywhere else, and it keeps compounding inside our ecosystem… Someone might say, ‘well, that’s all scrapable, isn’t it?’ Fact is that over 50% of the metadata underpinning a Rightmove listing is not scrapable from the face of our site”.

LLMs are only as good as the data that you feed into it. Real estate agencies may well be happy to provide a lot of this data directly to Chat GPT but this decentralizes much of the legwork of maintaining realtor websites and uploading data to individual realtor offices or companies which entails diseconomies of scale.

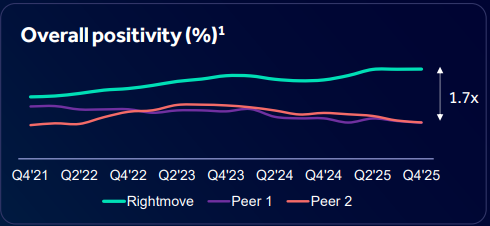

There is a narrative that Rightmove is a price-gouging monopolist, hated by its realtor customers, and this is corroborated by a £1bn lawsuit brought by a former Competition and Markets Authority (UK antitrust enforcement agency) panel member on behalf of estate agencies (and funded by a hedge fund). However, the data presented by Rightmove at least does not substantiate this dissatisfaction:

Finally, a property purchase/ sale is a highly emotive, well thought-through transaction. You are not looking for a quick answer. Before making a transaction you want to look carefully at the available options and alternatives. One might trust an LLM to tell you what is the best TV to buy for under $500 and might even give it your credit card details to buy it for you, but a property purchase is a different transaction entirely.

Conclusion

I have noted before and it is one of my core investing beliefs that price drives narrative, rather than the other way round. I suspect that much of the perception of real estate platforms as AI losers is correlated with declining share prices rather than a deep analysis of the business model and network effects of these companies.

By the same token, as these companies continue to perform, both in terms of continued growth & profitability as well as a stabilizing share prices, this will cause investors to reassess the bear case. Indeed at these valuations, time is on the long term investor’s side as every year of growth in excess of terminal g increases the net present value of cumulative cashflows.

Indeed in the case of Rightmove, the company will likely use cashflows to repurchase about 5% of the company’s shares. The business has no debt so could in fact be far more aggressive if they determine that fundamental value is well above the current stock market rating.

In sum, I believe Rightmove is one of the most compelling ideas in the market today, offering double digit returns in a base case scenario, and near 20% returns in a bullish case. Such returns for an exceptionally high quality, resilient company are rare in public markets. I have been adding to my position and it remains my 2nd largest holding.

Disclaimer

This article is purely for informational and entertainment purposes and should not be construed as investment advice. Please consult a financial advisor before making any investment decisions.

Please also assume that I own and intend to trade any stocks discussed before and after dissemination of this report.

Thanks for this. What a fascinating time to be a stockpicker. IF the AI threat is exaggerated, as I suspect, then this is a pretty rare opportunity to buy shares in outstanding companies like this, not to mention Constellation Software. But there's no guarantee, of course, and the waiting while being underwater is pretty stressful!

I guess it's not too dissimilar to what it must have been like buying Utilities and Consumer stuff etc. in 1999.

Really enjoyed this. Thanks for sharing. How you do think about OTM in the space ? Especially around pricing power. Thanks